Analysts have washed their hands of the stock. Goldman Sachs, JP Morgan and Citi have all sounded the selling horn on Asian Paints. Is this pessimism warranted, or will the stock take everyone by surprise?

Broad-based pessimism

The pessimism around Asian Paints is not limited to a select few analysts. Of the 38 brokers covering the stock, barely a handful – HSBC, HDFC, and Nuvama – are still positive on it. Only 16% are holding out a ‘buy’ signal, down from 26% at the start of the year and 41% a couple of years ago.

Also read: This small-cap has already gained 1,000%. Can AI fuel its next leap?

The stock has also been testing the patience of institutional investors. While domestic institutional investors (DIIs) have increased their stake in the company from 3.5% to 5.7% since September 2023, foreign institutional investors (FIIs) have been selling. FIIs’ shareholding in Asian Paints has dropped sharply from 17.7% to 12.2% over this period.

Stiff competition amid soft demand

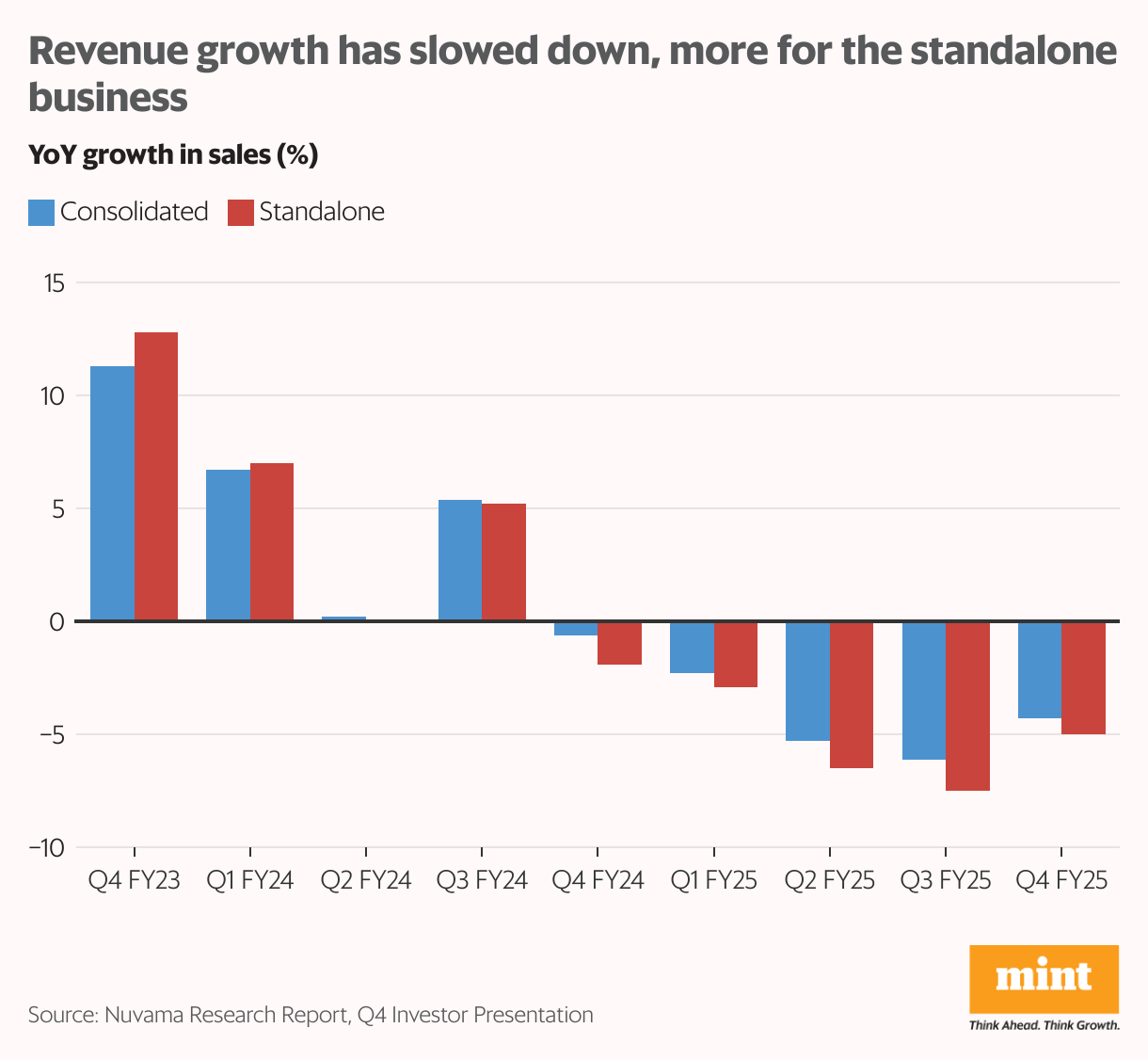

Asian Paints has long been synonymous with the Indian paints industry, commanding a 50% share of the market. But the industry has been under stress for several years now with demand slowing down and competition intensifying.

The company positions itself as a premium/luxury player for the most part. So, the recent urban demand slowdown has hit it where it hurts. Management has called out the current demand environment as the worst in two decades. Meanwhile, international business has been affected by currency depreciation in Africa, while the Industrials segment was mellow, too.

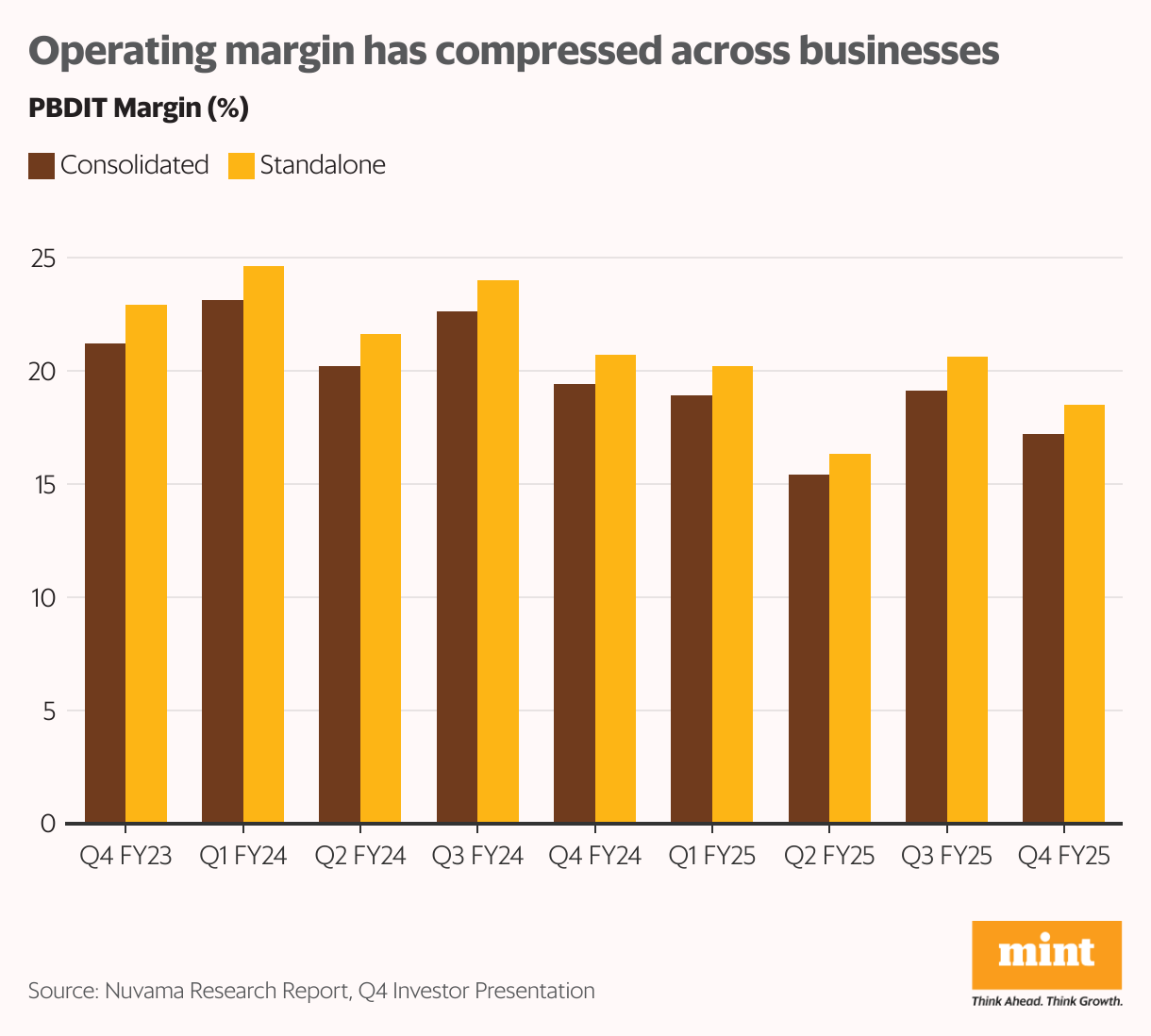

Despite gross margins holding steady around 43-44% over the years, operating margins have suffered due to negative operating leverage and higher spends on marketing and distribution. Even as management held back on cutting costs significantly to defend against competition, the profit before depreciation, interest, and tax (PBDIT) margin has fallen from 21% to 17% over the past couple of years.

Ceding ground in decorative paints

Decorative paints comprise around 70% of India’s paints industry. Repainting, which comprises 75% of the segment, has been affected by sluggish urban demand and downtrading by customers. Plateauing launches and residential projects have affected fresh painting as well.

According to an analysis by Anand Rathi, Asian Paints has ceded the most ground (350 bps) to new entrant Birla Opus. JSW Paints also presents a growing threat, particularly in Tamil Nadu, where Asian Paints is a market leader. But some loss in market share is par for the course for a dominant player when new players enter the arena. Moreover, Asian Paints’ dominance in tier-1 and tier-2 cities has left it more vulnerable to the recent slowdown in urban demand.

Also read: This textile star’s rally masks a margin meltdown. Should investors be worried?

The new entrants are capturing market share by tapping new dealers and offering significantly higher painter incentives and dealer margins – 10-12% against 4-5% for Asian Paints. Despite maintaining prices at the higher end of the industry range, negative operating leverage and higher spends on marketing and distribution have led to a margin compression for Asian Paints.

That said, the company has iterated that its value proposition remains unaffected by the new entrants, who do not offer any differentiated propositions. Long-term durability of the new players’ products remains untested as well.

Industrial segment has hurt profitability

In the industrial paints segment, Asian Paints operates through two joint ventures with PPG Inc., a global automotive coatings manufacturer. PPG-AP caters to a broad-based portfolio led by automotive clients, and comprises two-thirds of the industrial segment. AP-PPG constitutes the remaining third, and operates in the powder and protective coatings markets.

The latter accounts for more than 4% of the company’s revenues but less than 2% of its profits, and is thus margin-dilutive for the overall business. In FY25 the industrial segment saw decent 5% growth in revenues, thanks to factories and builder segments as well as a pickup in government spending in the second half of FY25. But, led by a 25% decline in profits for AP-PPG, the segment’s PBT saw 3% year-on-year degrowth.

International business flat

The international business has remained flat year-on-year as robust growth in the Middle East and a recovery in Asian markets has been negated by a sharp currency depreciation in the African markets of Egypt and Ethiopia.

As for profits, the company had to divest its Indonesia operations and recognise a loss of more than ₹80 crore. It also had to undertake a goodwill consolidation loss of more than ₹20 crore on a Sri Lankan acquisition. Overall, profits for the segment declined by 1.7% in FY25. The international business constitutes only about 10% of the company’s revenues and less than 3% of its profits.

Premium home décor offerings face headwinds

Asian Paints has partnered with Sleek for modular kitchens, acquired White Teak for decorative lighting and Weatherseal for doors and windows, and dominates the bath market with its Ess Ess brand. It also houses brands such as Nilaya, Royale and Ador, catering to furniture, furnishings, and lighting. It is also into interior designing through Beautiful Homes Service.

Also read: Can this under-the-radar company cash in on the $150 bn weight-loss drug boom?

The home décor segment contributes less than 5% to the overall business. It faces steady competition from unorganised players. Its kitchen segment reported flat revenues and accelerating losses owing to transition pains in the Sleek acquisition. White Teak, which procures a bulk of its inputs from China, saw a sharp 20% drop in revenues owing to new Bureau of Indian Standards (BIS) specifications. The company had to undertake an impairment provision of almost ₹80 crore because of this.

But the segments hold long-term potential, given the growing class of aspirational consumers. Supported by new launches of Beautiful Homes studios and stores, as well as successful collaborations with Sabyasachi, Jaipur Rugs and European designers, Asian Paints has grown as an integrated home décor player.

Silver linings

Asian Paints continues to command strong brand recall, and benefits from its efficient supply chains and expansive distribution network of 169,000 retail touchpoints. The company’s new economy-segment launches such as Ace and Tractor emulsions, and ‘Neo Bharat’ latex paints should support growth amid the slowdown in urban demand. But with a long-term view, 60% of its new products are likely to be in the premium to luxury space, thereby supporting margins. New products contributed 14% of revenues in Q4.

Asian Paints has also been investing in backward integration with white cement and VAM-VAE (vinyl acetate monomer and vinyl acetate-ethylene copolymer), which are key constituents of environmentally friendly and high-performance paints. They are currently imported, and local manufacturing would help improve cost efficiencies. This is expected to support margins while competition-led spending increases. The company has also been investing in digital solutions, innovation-led extended-warranty formulations, and sustainable products. These initiatives should reinvigorate its brand image, particularly among new-generation buyers.

Also read: This luggage leader is staging a turnaround. But can it overcome its baggage?

Q4FY25 saw some recovery in demand. Over the near term, moderation in crude oil prices and a stabilising rupee should support margins, especially as the company does not intend to pass on the benefits to consumers or dealers amid geopolitical uncertainty.

A recovery in urban demand and sustained rural demand could support growth going forward. Despite competitive pressures, which will eventually plateau, management has reiterated its guidance for 18-20% consolidated Ebitda margin. But the timeline is uncertain, and it is too early to call an end to the pressures of the past few years. The stock’s target price has been pegged at ₹2,282, at par with current levels.

For more such analysis, read Profit Pulse.

Ananya Roy is the founder ofCredibull Capital, a Sebi-registered investment adviser. X: @ananyaroycfa

Disclosure: The author does not hold shares of the companies discussed. The views expressed are for informational purposes only and should not be considered investment advice. Readers are encouraged to conduct their own research and consult a financial professional before making any investment decisions.