Timely rains boost farm output, lift rural incomes, and revive consumption in hinterlands—benefiting everything from FMCG to fertilizers, agri-machinery, and entry-level vehicles like two-wheelers and tractors.

Historically, the stock market has rewarded companies with strong rural linkages when the monsoon arrives on time. With pre-monsoon showers already underway, select stocks are well-positioned to ride this seasonal tailwind.

Here are three such companies with rural exposure, solid fundamentals, and potential to outperform as demand picks up.

#1 Godrej Agrovet

Godrej Agrovet is a diversified agri-business company with interests spanning animal feed, crop protection, oil palm, and dairy.

As one of the leading players in India’s rural economy, the company stands to benefit directly from the onset of monsoon, which typically drives higher agricultural activity and rural income.

The company operates across five key business verticals, all directly serving or interacting with the agricultural sector and rural communities, namely animal feed, crop protection, oil palm, dairy and poultry and processed foods.

With pre-monsoon showers already underway, the company is well-placed to benefit from a rural resurgence.

The management has also indicated a positive outlook for the upcoming year citing improved demand visibility, stable input costs, and ongoing turnaround efforts across key segments.

For FY26, the company is guiding for 16-18% in top-line growth, primarily driven by volume growth rather than inflation. Profitability is also expected to grow at a similar pace with a significant portion coming from the reduction of losses in Astec LifeSciences, its CDMO business.

The company anticipates reducing its loss in Astec LifeSciences to less than half of the previous year’s loss on a conservative basis, which is expected to drive overall profitability.

While the outlook is now turning positive, it follows a period of subdued performance.

Over the past five years, Godrej Agrovet’s revenue and net profit have grown at a modest compounded annual growth rate (CAGR) of 6%. This has been due to a mix of factors including changes in commodity prices, demand-supply imbalances, and strategic shifts within the company.

Margins have also witnessed fluctuations with operating profit margins declining from 9% in FY21 to a low of 5.6% in FY23 and net profit margins dropping from 5% in FY21 to 3.2% in FY23.

However, over the last two years, the company appears to have emerged from this low-margin phase. It is now in a period of margin recovery and operational stability.

For the financial year 2025, Godrej Agrovet reported its highest-ever standalone net profit, driven by an exceptional performance in the domestic crop protection and vegetable oil businesses, along with margin expansion in the animal feed segment.

The company’s operating profit margin also improved to 8.7%, from 7.4% in FY24, despite flat revenue growth.

Return ratios have also followed a similar trajectory. After a temporary dip in FY24, return on equity (RoE) and return on capital employed (RoCE) both have rebounded to 16.5% in FY25 on the back of an increase in profitability.

This financial turnaround has been mirrored in the company’s market performance. Godrej Agrovet’s stock has rallied over 60% in the past year, signalling renewed investor confidence.

As a result, it now trades at a price-to-earnings (P/E) ratio of 37x, about 12% above its 10-year average of 33x.

For investors looking for a stock with a strong rural footprint and improving profitability, and a potential monsoon tailwind, Godrej Agrovet offers an interesting case.

However, with the stock currently trading at a premium, near-term upside may be limited unless growth accelerates meaningfully, making it more suitable for long-term investors who believe in the company’s structural story and operational turnaround.

Also Read: This small-cap has already gained 1,000%. Can AI fuel its next leap?

#2 Coromandel International

As one of leading agri-solutions providers in the country, Coromandel International is also well-positioned to benefit from a strong pre-monsoon season.

The company is one of India’s leading agri solutions provider that offers a diverse range of products and services across the farming value chain.

It specializes in fertilizers, crop protein, bio pesticide, specialty nutrients, organic fertilizers, etc that usually see heightened demand ahead of sowing activity.

With farmers typically ramping up fertilizer purchases in anticipation of good rainfall, Coromandel could see strong volume growth, supporting both topline momentum and margin expansion simultaneously.

The company is the largest single super phosphate player in the domestic market and the second-largest player in other complex phosphatic and potassium market. It has also holds a 53% stake in NACL Industries (worth ₹820 crores), a renowned player in the agricultural space.

The company recently acquired shares of the company in an effort to augment its crop protection portfolio. The acquisition is expected to strengthen its presence in the domestic formulations business, and also expand its existing product portfolio.

Going ahead, the management expects favorable weather forecasts for the upcoming kharif season in key operating markets to support its business.

It also remains bullish on the agri input sector, citing positive turnaround in the agricultural sector, strong policy support, and favourable monsoon forecasts.

The company is making significant capital expenditures on backward integration projects for phosphoric acid and sulfuric acid, as well as a new granulation train, to enhance its fertilizer production capabilities.

It has also planned expansion of capacities in crop protection active ingredients and debottlenecking fertilizer facilities. These investments are expected to the demand from the agricultural sector.

With respect to financials, Coromandel International has demonstrated a steady growth trajectory over the last five years.

The company’s revenue has grown at a compounded annual growth rate (CAGR) of 13% on the back of the company’s robust market position in India’s phosphatic-fertilizer market while net profit has grown at 11% on account of its strong operating efficiency.

Operating margins have also been largely stable in this period, hovering between 10% and 14%, with a peak in FY21.

While operating profit margins dipped to 11% in FY25, the company expects this to turn around going forward as it plans to focus on leveraging synergies (with the NACL acquisition) and scaling up high-margin segments like speciality nutrients, nano DAP, and retail.

Return ratios have also remained robust with return on equity (RoE) averaging at 22.1% and return on capital employed averaging at 31.2%.

Coromandel has cash and cash equivalents of ₹3,538 crores as of 31 March 2025. This is more than enough to cover its annual capex of ₹800-1,000 crores and other expenses.

The acquisition of NACL, worth ₹820 crores and an incremental working capital requirement over the medium term, will be met through strong yearly cash accruals of ₹1,500-1,700 crores.

As a result, the company is expected to remain net debt free over the medium term.

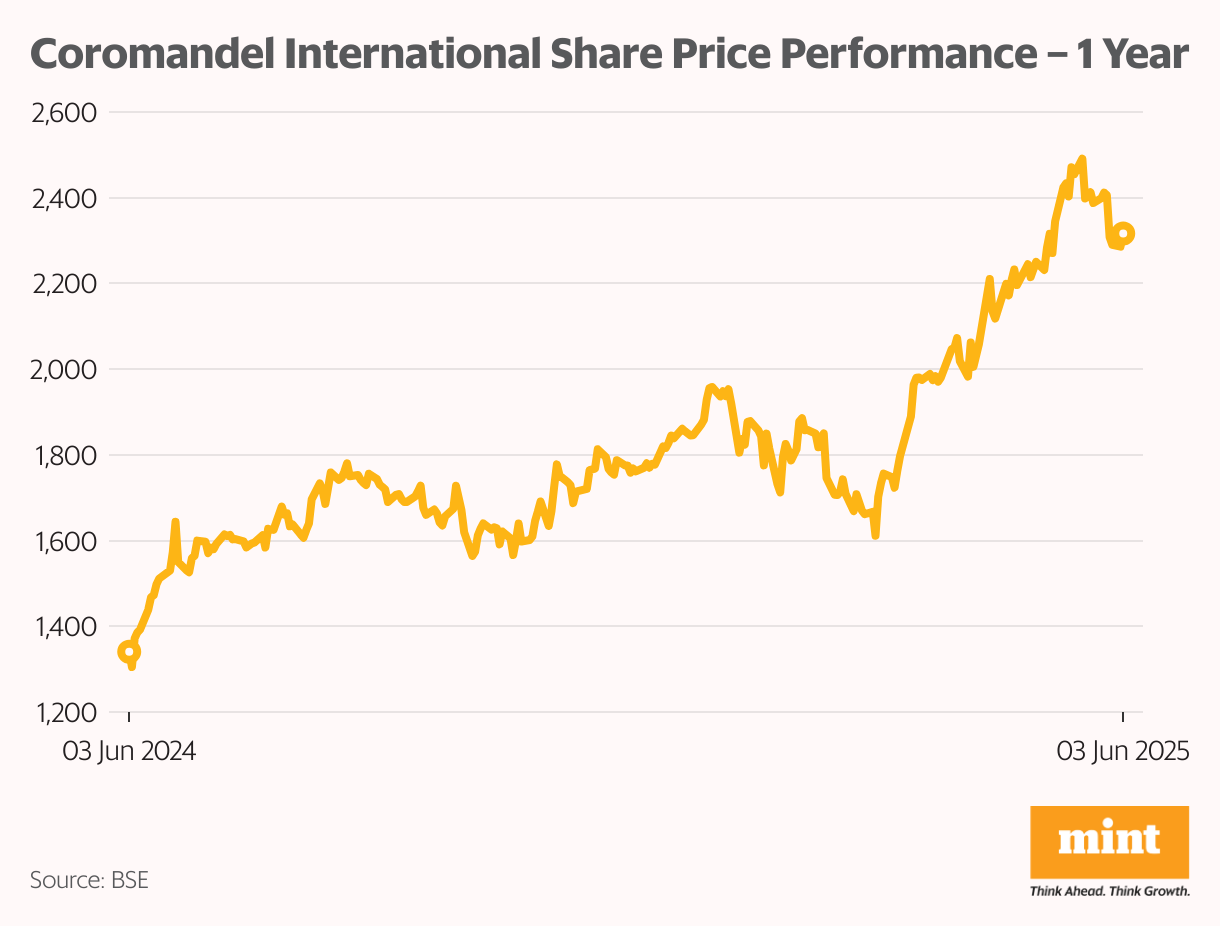

Shares of Coromandel International have risen over 30% over the last six months and over 70% over the past year on account of its strong financial performance.

FIIs have also shown renewed interest in the company, with their stake rising from 7.18% in September 2023 to 10.61% in March 2025, the highest level.

As a result of this rally, the stock is no longer cheap. It currently trades at a price-to-earnings ratio of 38x, a 111% premium to its 10-year average PE of 18x.

Also Read: FMCG stocks face margin pressure. Here’s why

#3 Hero Motocorp

While Hero MotoCorp’s business is not directly linked to the monsoons, the company derives over

50% of its from rural and semi-urban markets, which typically see a pickup in demand following good rainfall.

A favorable monsoon boosts farm incomes and improves cash flows, which in turn enhances consumer sentiment and drives up sales of commuter motorcycles and scooters.

As a result, the company is expected to gain immensely from the pre-monsoon showers, making it a strong proxy for India’s monsoon-driven consumption recovery.

The company’s management has already indicated optimism about the recovery of the broader two-wheeler market in rural and urban areas, influenced by a better monsoon.

Hero MotoCorp is particularly equipped to capture this demand, thanks to its extensive product portfolio and deep rural distribution network.

The 100cc/110cc motorcycle segment, which forms the backbone of the Indian two-wheeler industry, is a stronghold for the company. Hero expects this segment to perform well, especially in rural areas, and contribute meaningfully to overall growth.

Management is confident of outperforming the industry in FY26, citing strong Q4, new launches, rural recovery, and export momentum.

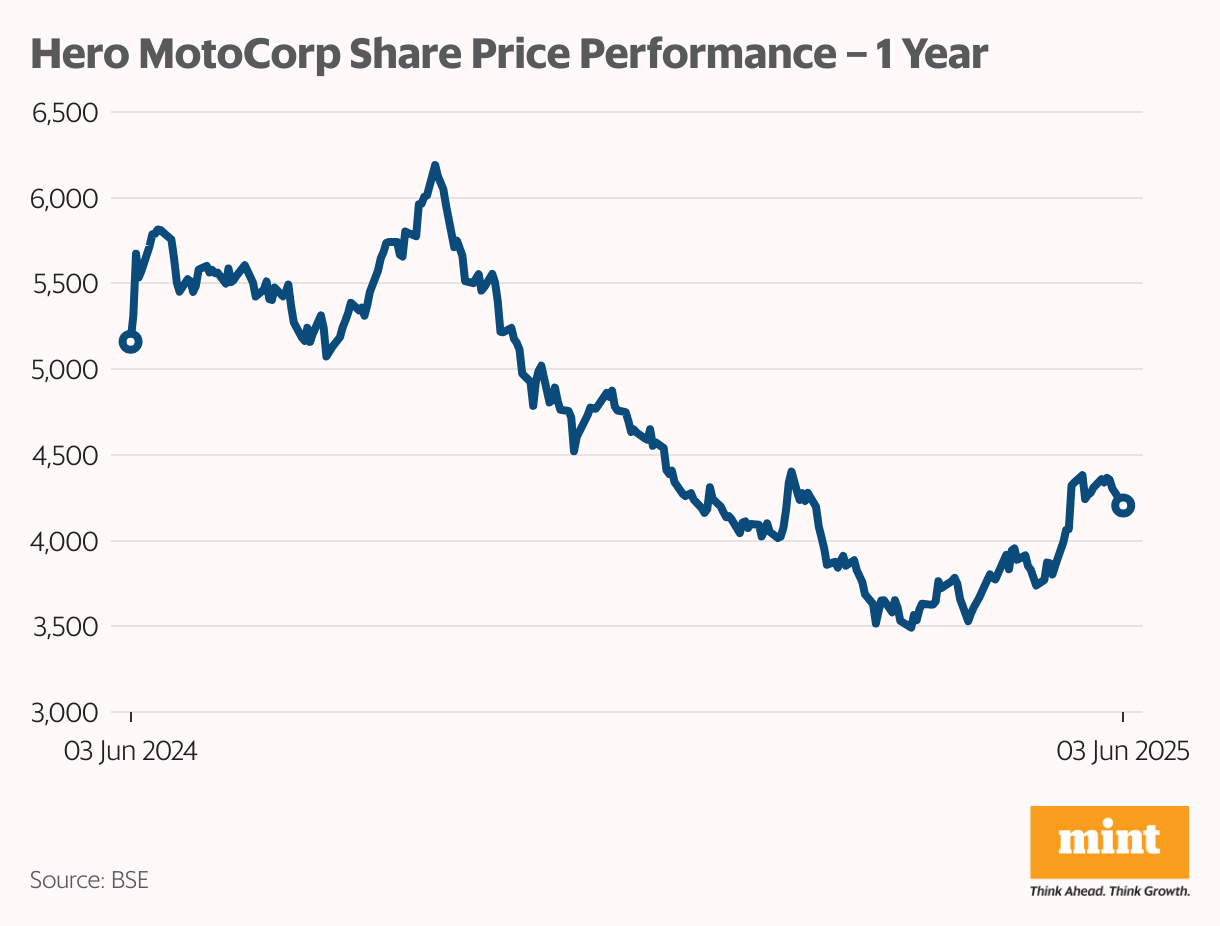

However, the stock has underperformed in recent months. Shares of Hero MotoCorp are currently down over 10% over the last six months and 18% as concerns around shrinking market share and challenges in the premium and electric vehicle (EV) segments have weighed on investor sentiment.

As a result, the stock is trading at PE ratio of 19x, 10% below its 10-yr PE of 21x.

However, the company plans to turn this around in the upcoming quarters. To gain traction in the premium market, the company is ramping up brand-building efforts and launching high-end models, including those from its Harley-Davidson partnership.

On the EV front as well, the company is expanding its mass-market lineup with the Vida V2 platform. It is also venturing into the three-wheeler EV segment through an investment in Euler Motors, signalling an intent to grow both organically and inorganically.

Despite market share pressures, the company’s financial performance has remained solid. Over the past four quarters, the company has posted consistent revenue and profit growth, driven by strong sales.

For FY25, the company reported its highest ever revenue at ₹40,923 crores driven by higher exports and strategic global expansions while net profit jumped 17% YoY to ₹4,376 crores.

It also retained its global leadership as the largest motorcycle & scooter manufacturer for the 24th consecutive year.

This jump in profitability has translated into robust return ratios for the company. The company’s RoE stands at 23.7x while RoCE at 31.2x, above many of its peers.

It also maintains a robust balance sheet, with a near-zero debt-to-equity ratio of 0.02x, ensuring financial stability even as it navigates an evolving market.

Also read: This textile star’s rally masks a margin meltdown. Should investors be worried?

Conclusion

The onset of pre-monsoon showers often acts as a trigger for renewed optimism in rural-focused sectors.

Afterall, a good monsoon translates into stronger farm output, improved rural incomes, and a lift in consumption across categories from agri-inputs to entry-level two-wheelers.

However, despite the massive upside, investors should remain cautious. Weather patterns can be unpredictable, and even a brief disruption in rainfall can delay or mar the expected demand recovery.

Company-specific headwinds like input cost pressures and market share concerns can also impact financial performance, regardless of seasonal trends.

As always, it’s important to look beyond near-term triggers and evaluate the underlying fundamentals. A financially strong business is more likely to deliver sustainable returns than one driven solely by seasonality.

For more such analysis, read Profit Pulse.

Ayesha Shetty is a research analyst registered with the Securities and Exchange Board of India. She is a certified Financial Risk Manager (FRM) and is working toward the Chartered Financial Analyst (CFA) designation.

Disclosure: The author does not hold shares in any of the companies discussed. The views expressed are for informational purposes only and should not be considered investment advice. Readers should conduct their own research and consult a financial professional before making investment decisions.