Yet amid the selloff, contrarian investors are spotting opportunities.

There are plenty of reasons for optimism. Global IT spending is projected to rise 9.3% in 2025, driven by double-digit growth in software and data center segments, according to Deloitte. The rapid adoption of artificial intelligence (AI) technologies across industries is further boosting demand for cloud infrastructure and AI-enabled services.

While near-term challenges persist, the long-term outlook for Indian IT stocks remains bright. Against this backdrop, we’ve identified five undervalued IT stocks to watch closely.

#1 Infosys Ltd

First on the list is Infosys Ltd.

Infosys, a leader in global IT services, consulting, and outsourcing, also provides critical infrastructure management services such as cloud migration, server network maintenance, and cybersecurity.

The company’s digital push spans AI, cloud computing, and data analytics, modernizing client operations. However, revenue and profit growth have been flat over the past two years, with FY25 net profit up just 1.9% year-on-year.

Despite near-term headwinds from spending cuts and geopolitical risks, Infosys is building for the future. It is developing autonomous AI systems to enhance enterprise resilience, expanding its cloud services (which contribute 30% of revenue and are growing 25% annually), and boosting its edge computing and 5G capabilities.

Read this | Can Infosys weather this storm better than peers?

Valuations remain attractive, with Infosys shares trading below peers and offering a dividend yield of nearly 3%.

#2 HCL Technologies Ltd

HCL Technologies, India’s third-largest IT firm by revenue, has taken early leadership in enterprise AI adoption, with most of its earnings driven by software development, infrastructure management, and business process outsourcing.

Despite industry pressures, HCL Tech has seen steady growth. The company reported 10.8% net profit growth in FY25, outpacing peers, though revenue growth was modest at 6.5%.

Looking ahead, HCL is expanding its use of generative AI across banking, healthcare, and manufacturing, with strategic collaborations with Google Cloud and Microsoft for AI infrastructure.

HCL Tech plans to capitalize on growth opportunities in AI, semiconductors, and edge computing, while aligning with global trends in sustainability and cybersecurity. Its $300 million semiconductor investment and focus on TX make it well-positioned to tap into India’s growing tech ecosystem and meet evolving enterprise demands.

The stock is trading at a PE ratio of 24, below the industry average of 28.

Next on the list is Birlasoft.

Founded in 1990, Birlasoft is a leading global IT services firm headquartered in Pune, Maharashtra, India, and is part of the diversified CK Birla Group. The company blends deep domain expertise with cutting-edge enterprise and digital technologies to help businesses reimagine their processes and unlock new growth opportunities through digital transformation.

While Birlasoft continues to leverage its strengths in emerging technologies and digital transformation, its third-quarter performance for the period ending 31 December 2024 fell short of expectations. Net profits dropped 27.4% on year to ₹1,169 million, impacted by higher employee costs and a seasonally subdued demand environment.

Despite a challenging start to FY25, marked by weaker revenue and margins—primarily due to furloughs in sectors like life sciences and manufacturing—Birlasoft remains optimistic about its strategic roadmap to boost profitability and scale its global operations.

Over the next 1–2 years, the company plans to invest heavily in expanding its global footprint, targeting new markets to diversify its client base. Birlasoft is also set to continue leveraging its expertise in digital transformation and emerging technologies to create client value and strengthen its market position.

The stock is currently trading at a PE ratio just under 20, which is attractive relative to its peers.

Wipro Ltd, a leading Indian multinational technology company headquartered in Bengaluru, provides IT services, consulting, and business process outsourcing across 65 countries.

Wipro outperformed its peers in Q4FY25, reporting strong quarterly results. Large deal bookings surged 48.5% year-on-year (YoY) to $1.76 billion, signaling a robust pipeline, while total contract value (TCV) bookings reached $3.96 billion, up 13.4% sequentially in constant currency.

Several factors contributed to Wipro’s strong quarter, including a 26% YoY rise in net profit and stable margins despite modest revenue growth. The company’s performance was driven by strong large deal bookings, cost control that maintained margins, growth in key verticals, and a strategic emphasis on AI. These factors helped mitigate softness in certain sectors and geographies.

Looking ahead, Wipro is intensifying its focus on large strategic accounts in key sectors, with a solid pipeline of major deals, including a recent £500 million contract with the UK’s Phoenix Group.

The company has realigned its Global Business Lines (GBLs) to prioritize AI, cloud, digital transformation, cybersecurity, and industry-specific cloud solutions. Effective from April 2025, this restructuring aims to deliver integrated, outcome-driven solutions that enhance client agility and innovation.

Wipro shares are currently trading at a PE ratio of 20.

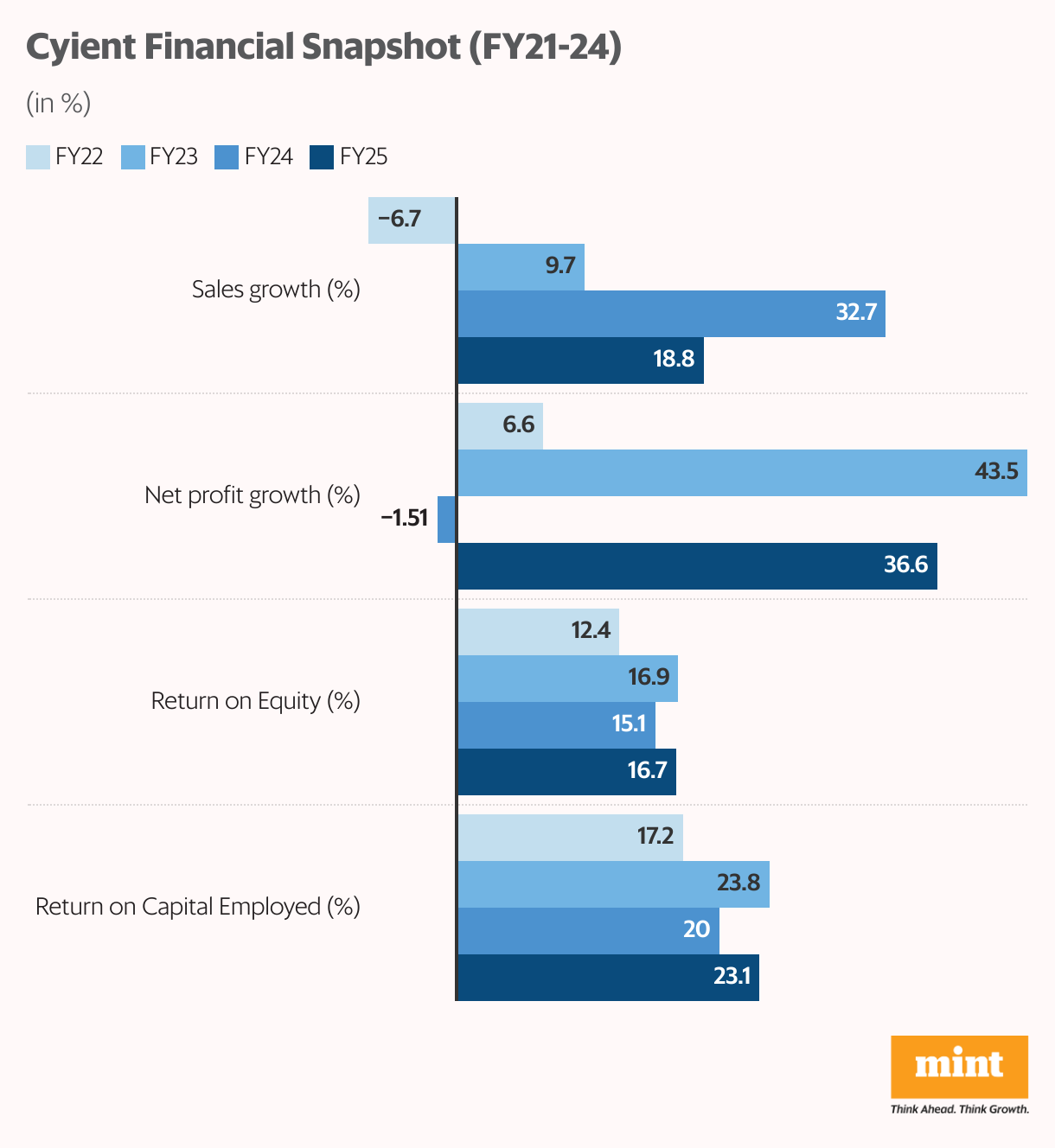

Next on the list is Cyient.

Cyient is a global engineering and technology solutions provider headquartered in Hyderabad, India. Operating across North America, Europe, Asia-Pacific, and India, the company serves more than 300 customers worldwide, including 30% of the world’s top 100 innovators.

The company has experienced steady growth in recent years, with FY24 being particularly strong. However, for the quarter ended 31 December 2024, Cyient reported a subdued performance, with consolidated net profit falling 16.2% YoY to ₹1,284 million, down from ₹1,532 million in the same period the previous year.

Despite this, Cyient is seeing robust order intake growth, with a 5% YoY increase in Q3 FY25. The company continues to expand its presence in aerospace, connectivity, and emerging sectors like semiconductors and automotive electronics.

In April 2025, Cyient launched Cyient Semiconductors, a wholly owned subsidiary focusing on scaling Application-Specific Integrated Circuit (ASIC) turnkey solutions. Leveraging over 25 years of semiconductor design expertise, this subsidiary operates across India, the US, Germany, Belgium, the Netherlands, and Taiwan.

These developments position Cyient for strong future growth. The stock is currently trading at a PE ratio of 21.

Conclusion

Massive corporate spending on AI infrastructure and accelerated computing is driving demand for specialized semiconductors and software platforms. Enterprises are increasingly adopting cloud solutions, digital automation, and AI technologies, benefiting companies offering cloud infrastructure, SaaS, and digital consulting services.

Also read | In charts: Sombre mood grips India’s top IT firms amid tariff tantrums

The convergence of AI advancements, cloud modernization, and pent-up enterprise demand presents a strong growth outlook for IT companies—especially those balancing innovation with operational resilience.

Investors should carefully evaluate company fundamentals, governance, and stock valuations when conducting due diligence before making investment decisions.

Happy investing.

Disclaimer: This article is for information purposes only. It is not a stock recommendation and should not be treated as such.

This article is syndicated from Equitymaster.com